Today’s expensive housing market and high interest rates make it challenging for people to attain homeownership. Furthermore, high closing costs (which include the nonnegotiable premiums for title insurance) have created an additional barrier for homebuyers. Typical loan closing costs have risen almost 22% between 2021 and 2022, according to the Consumer Financial Protection Bureau. In its inception, title insurance’s purpose was to protect homeowners and mortgage lenders. However, today it stands as an unnecessarily high cost that does not reflect the actual cost to insure title risk. This policy brief examines the history of title insurance and recent policy proposals to amend how it is sold and regulated. We support the proposed bills that establish a state-run title insurance program and believe that excess proceeds from the program should fund affordable homeownership initiatives.

Title insurance began in the late 19th century, when property transactions were risky due to unclear or disputed land titles. Public records were limited then, and property ownership records were often incomplete or inaccurate. However, as the industry grew and the country urbanized, title insurance companies expanded their services and became a standard component of real estate transactions to protect owners and mortgage lenders from unknown defects in the title to a property. While there are still hundreds of title insurance companies around today, the industry has consolidated around four companies which collectively own more than seventy percent of the market share. This non-competitive market disadvantages consumers and allows the major companies to drive up costs by establishing excessive premiums that do not match the risk or cost.

Title insurance rates and pricing are typically regulated by each state. In New York, the Title Insurance Rate Service Association or TIRSA, which is comprised of members of the title insurance industry, is licensed by the Department of Financial Services (DFS) to develop and file title insurance rates, policy forms, and endorsements on behalf of its member insurers. DFS authorizes TIRSA to propose title insurance rates for DFS review and approval. Unfortunately, TIRSA has struggled to manage the relationship between real estate attorneys, realtors and lenders, and their member title insurance companies. For example, in 2015, DFS found that title insurance companies spent millions of dollars on meals, entertainment, and unreported gifts to incentivize attorneys, agents, and lenders to direct business to their title companies, adding costs that inflate the overall price. This dynamic creates reverse competition and warped incentives, where the product is not marketed to the purchasers, but rather intermediaries. In the aftermath of the investigation, DFS issued regulations in an attempt to curb these unscrupulous practices; however the cost of title insurance has since continued to rise. In fact, acquiring property in New York comes with some of the highest title insurance premiums in the country due to the outsized market value of homes. Recent analysis shows that New York State has an average cost of about $3,500, while in New York City, the average title insurance cost is about $5,500.

Attempts to address this have found varying levels of success. In 2015, then-U.S. Representative Keith Ellison (D-MN) introduced H.R. 1799, the Ensure Fair Prices in Title Insurance Act, which prohibited financial benefits for referrals at the federal level, but the bill failed to gain traction in the Congress. However, state-level efforts that followed were more successful. New York, for example, passed anti-inducement regulations to rein in kickbacks and other improper expenditures that same year. Later, in 2017, DFS further refined these regulations to clarify and strengthen the anti-inducement statute. Despite these regulations, the industry remains opaque, with high rates that do not reflect the insurance cost or payouts, as we will prove below.

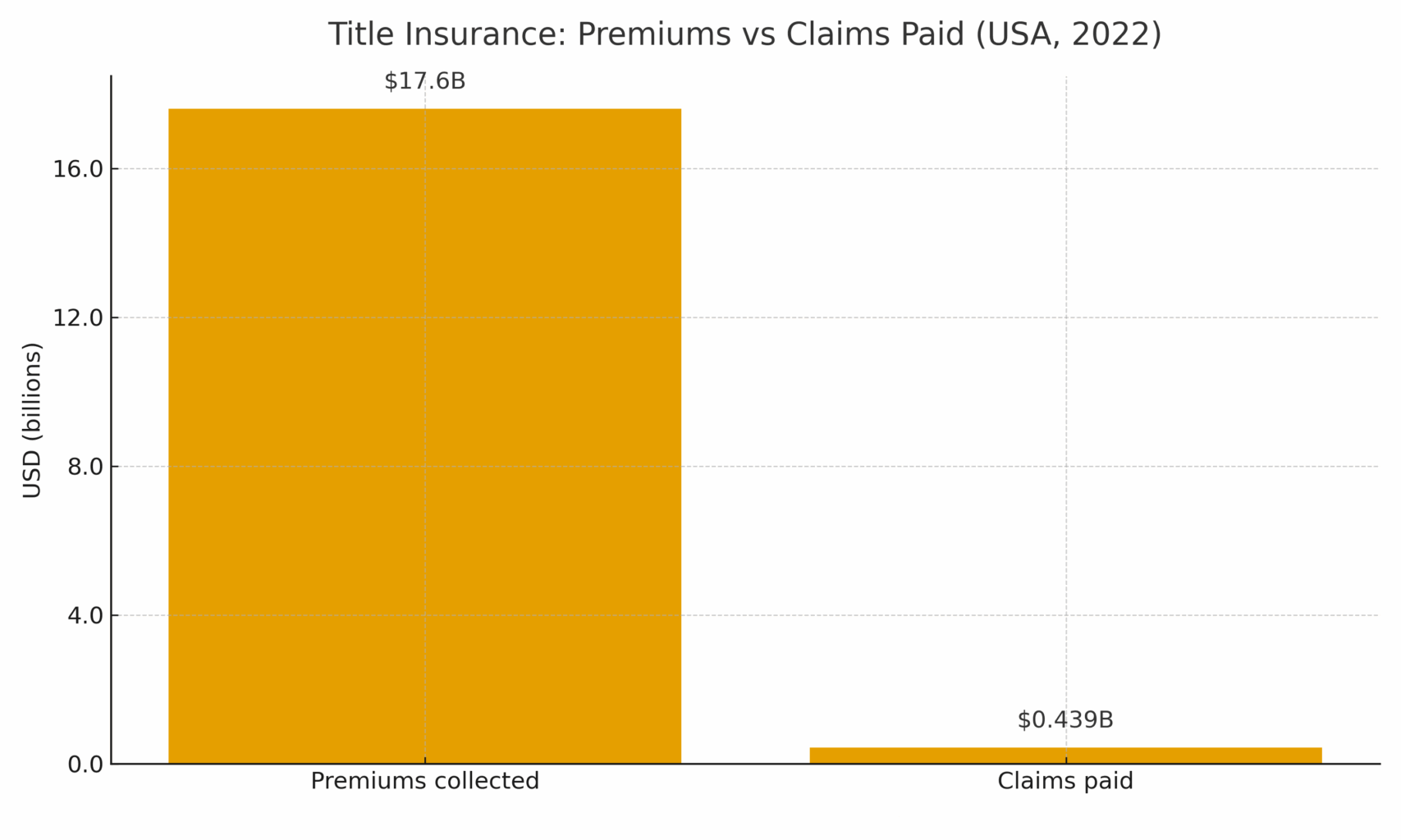

A national GAO investigation in 2007 questioned whether premium rates reflect underlying costs and how the market’s lack of regulation, and lack of competition, led to price inflation. These issues have persisted today, with title insurers bringing in $17.6 billion in premiums and paying out $438.6 million in claims in 2022 (see figure 1). This is a payout rate of 2.4%, compared to property and casualty insurers, who spend over 70% of their revenue on claims for losses like house fires and vehicle accidents.

Figure 1 – Comparing the total amount of title insurance premiums collected to the total amount title insurance paid out in 2022.

An additional factor driving up costs is that the cost of the insurance is not tied to the complexity of the title search, but rather the sale price of the home and mortgage for the bank. If title insurance rates reflected the structure of other types of insurance – driven by pay out risks and complexities — premiums would be less than a tenth of average national rates. This would take a typical rate from 0.5% of a home’s purchase price to 0.05% of the home price. Therefore, reducing these costs could save the median borrower $5,000-10,000 in upfront costs. As the Urban Institute reports, savings of this scale not only make purchasing a home easier and more in reach but also give prospective homebuyers a better chance at preventing future defaults.

State action and enhanced regulations in Iowa have been proven to successfully reduce title insurance costs. For example, Iowa runs a state-owned title guarantee program called Iowa Title Guaranty (ITG). The state forbids commercial title insurance, and instead offers coverage for residential property at a flat fee of $175 for transactions of $750,000 or less. ITG is comparable to traditional private title insurance, yet it manages to keep premiums much lower than a comparable private title insurance policy. With a premium rate between 0.10% – 0.15% of the purchase price for residential properties, ITG’s charges are minor compared to New York’s rate of 0.75% of the purchase price, yet still cover their costs. Additionally, ITG requires that issues with titles be resolved before closing, which helps to prevent outstanding issues and keep claim rates low. The result is that Iowa has the lowest claim rates in the country, typically sitting at 1% or lower.

Importantly, ITG passes a portion of the fee to attorneys and abstractors, with no money going to the lender, which eliminates the kickback problem seen in other states like New York. Furthermore, any excess revenue beyond operating expenses is given to affordable housing initiatives in Iowa, such as helping first-time homebuyers with a down payment, paying down interest on a mortgage loan, and funding free foreclosure prevention services. Iowa estimates that between $1 million and $2 million of their revenue annually ends up going to these causes – totalling $68.5 million since the agency’s inception.

In New York, current legislative efforts to reform title insurance resemble components of the Iowa program and provide further structure and guidance to regulate the industry. Like the Iowa program, two current state bills (S1082 and A3818) would create a government-administered title coverage program to provide affordable protection for homebuyers and put revenue generated from title insurance into a “title guaranty fund” to support affordable housing initiatives.

Drawing further inspiration from Iowa, the two New York bills create a new state corporation, the New York Title Guaranty Corporation, which will work in consultation with state agencies like DFS, to implement its programs as well as set a fixed price for title protection for real estate owners and lenders. One bill (S4539/A4500) goes even further, establishing a statewide electronic database of real property to help participating abstractors and attorneys working within the title guarantee program.

Revenues from the proposed New York Title Guaranty will go beyond the program’s impact on individual real estate transactions by funding affordable housing initiatives. Specifically, bill S4539/A4500 establishes a fund, jointly managed by the New York Title Guaranty Corporation and the state comptroller, which will collect money from the program to cover the program’s administrative costs, and also support the Homeowner Protection Program – the country’s the largest and most successful foreclosure and deed theft prevention program and a gem in the NYS social safety net. Not only do these title insurance reforms curb accelerating costs of title insurance, they also provide permanent and much-needed funding for legal defense and affordable housing initiatives that keep New Yorkers safely housed and building equity.

While title insurance is crucial for securing property transactions, its current costs and regulatory inefficiencies impose a significant financial burden on homebuyers. Iowa’s successful state model, with its fixed pricing and effective use of excess funds, provides a valuable blueprint. New York’s proposed reforms, which include establishing a state-run title insurance program and directing excess revenue to affordable housing, are promising and much-needed steps that would advance our reputation as a state with a sophisticated, holistic approach to consumer protection. Until federal intervention standardizes practices nationwide, New York and other states must continue to lead the way in creating a fairer, more transparent and more affordable title insurance model that builds communities and intergenerational wealth instead of padding the bank accounts of four corporations.

Dial 311 and ask for the Center for NYC Neighborhoods

Or call us directly at 646-786-0888

Email: info@cnycn.org

Press: press@cnycn.org